The Real Cost of Client Acquisition for RIAs in 2026

- May 14

- 8 min read

A channel-by-channel breakdown of what RIAs actually pay to acquire a new client — and why most published CAC numbers in wealth management are wrong.

By Ian J Karnell, CEO & Co-Founder, VastAdvisor — May 2026

Ask ten RIA principals what their cost to acquire a client is and you'll get ten different answers. Ask them how they calculated it and the answers get worse. The number most firms quote is some mix of last-touch attribution, fully unloaded marketing spend, and a referral economy that gets categorized as "free." None of it survives a finance meeting.

This matters more than it used to. The firms running real growth programs in 2026 — the ones treating acquisition as infrastructure rather than as a series of one-off campaigns — are operating with 30–60% lower CAC than the industry baseline, and they got there by being honest about what each channel actually costs. The firms still working off back-of-envelope numbers are quietly losing share every quarter.

This piece does three things. First, it walks through what each major acquisition channel actually costs an RIA in 2026, fully loaded. Second, it explains why the standard CAC numbers in wealth management are misleading and what to use instead. Third, it lays out which channel mix wins over a five-year horizon — and which one is a tax most firms are unknowingly paying.

Why most published CAC numbers in wealth are wrong

Three reasons, in order of severity.

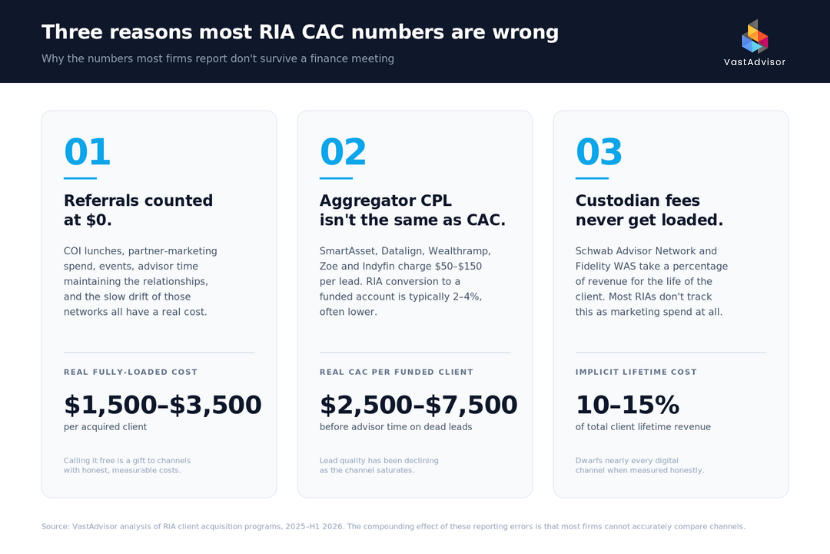

Referrals get counted at zero. They're not. A center-of-influence program — the CPAs and attorneys feeding most "free" referrals — has a fully loaded cost when you account for the lunches, the events, the partner-marketing investment, the case-by-case advisor time, and the slow drift of those relationships requiring constant maintenance. A reasonable estimate for a referral-driven RIA is $1,500–$3,500 per acquired client when you actually load the program. Calling it free is a gift to channels that have real costs.

Paid lead aggregators get counted on cost-per-lead, not cost-per-funded-account. SmartAsset, Datalign, Wealthramp, Zoe, Indyfin and their peers typically charge $50–$150 per lead. The conversion rate from those leads to funded accounts is 2–4% in most RIA programs we see — sometimes lower. Multiply through and the real CAC on aggregator channels lands at $2,500–$7,500 per funded client, before you factor in the time advisors burn working unqualified leads.

Custodian referral programs get treated as marketing spend rather than revenue share. Fidelity Wealth Advisor Solutions and Schwab Advisor Network are not free. The lifetime referral fee — typically a percentage of revenue for the duration of the relationship — is the single most expensive form of "marketing" most RIAs are running, and it doesn't show up as a marketing line item. On a 20-year client relationship, the implicit CAC can run 10–15% of total client lifetime revenue, which dwarfs anything you'd ever pay a digital channel.

If you stop there and just stop double-counting, your CAC reporting gets dramatically more honest. Most firms don't, which is why most firms can't tell you which channel is actually working.

Channel-by-channel: what it really costs an RIA in 2026

Numbers below are typical ranges from RIA programs we've reviewed across 2025 and the first half of 2026. Variance is high — the gap between a well-run channel and a poorly run one is often 3–5x. Treat these as anchors, not benchmarks.

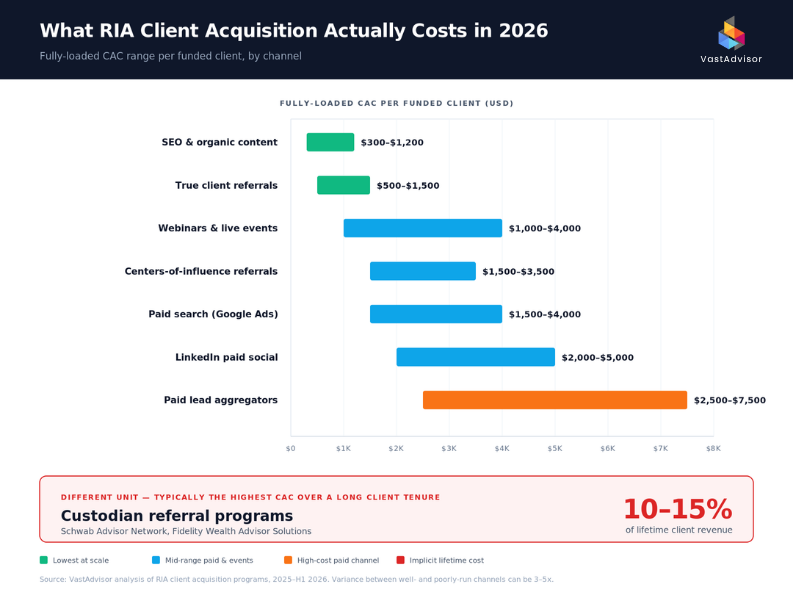

Centers-of-influence referrals — fully loaded CAC of $1,500–$3,500 per funded client. Doesn't scale linearly with effort. Quality is high; the model is fundamentally networked, which means it caps at the size of the network.

Paid lead aggregators (SmartAsset, Datalign, Wealthramp, etc.) — $2,500–$7,500 per funded client after conversion. Lead quality is mixed and trending down as the channel saturates. The aggregators are also competing directly with their own RIA buyers in some configurations, which is a real concern most RIAs don't price into the channel.

Custodian referral programs (Schwab Advisor Network, Fidelity WAS) — 10–15% of lifetime client revenue as an implicit CAC. High quality, low-effort to receive, but the most expensive channel in the long run if you don't factor the fee in. The math gets ugly fast on long client tenures.

Paid search (Google Ads on advisor-intent keywords) — typical CPC of $30–$100 on terms like "fee-only financial advisor [city]," with conversion to qualified consultation at 2–8%. Fully loaded CAC: $1,500–$4,000 per funded client when run well, $8,000+ when run badly. Highly dependent on landing-page quality and follow-up speed.

Paid social — LinkedIn — $25–$75 CPC on wealth-relevant audiences, with cost per qualified MQL in the $200–$500 range. Conversion to funded account 5–10% on warm flows. Strong for enterprise and high-net-worth targeting; weak for mass-affluent.

Paid social — Meta / Instagram — much cheaper top of funnel ($1–$5 CPC) but weaker advisor-intent signal. Best used as a retargeting and content-amplification channel, not a primary acquisition layer for full-fee RIAs.

SEO and organic content — slowest channel to spool up (9–18 months for compounding effect), and the cheapest at scale once it does. Fully loaded CAC at maturity: $300–$1,200 per funded client for firms that have built real topical authority. The catch: most RIAs never get to maturity because they treat content as a one-quarter experiment.

Webinars and live events — highly variable, typically $1,000–$4,000 per funded client when you fully load production cost, list-building, and follow-up time. Strong for warming a defined ICP. Useless if your ICP isn't tight.

Podcasts and earned PR — almost impossible to attribute directly. The right way to score these is on assisted conversions and on the lift they provide to branded search volume. Run them as a brand and authority channel, not a CAC line item.

True organic referrals (existing-client introductions) — usually the cheapest channel by a wide margin: typically $500–$1,500 fully loaded, when you account for the client-experience investment that produces them. The constraint is volume, not cost.

The pattern is consistent: there is no single "right" CAC for an RIA. There is only the right blend of channels for your firm's stage, ICP, and time horizon.

The CAC math you should actually be running

Three numbers matter. Most firms aren't tracking any of them.

CAC-to-funded-account. Stop reporting cost per lead. Cost per lead is a vanity metric. Report cost per funded account. The difference between $100 CPL and $7,000 CAC-per-funded-account is the entire conversation.

CAC payback in months. How long until the new client's recurring fee revenue exceeds what you spent to acquire them? For most RIAs, this should be under 18 months. If it's not, the channel is buying revenue you don't actually keep.

CAC as a percentage of LTV. Healthy RIAs operate at CAC-to-LTV ratios of 1:5 to 1:15 depending on segment. Below 1:5 and you're overpaying; above 1:15 and you're under-investing in growth. The custodian referral channel routinely runs at 1:2 to 1:4 once you load the lifetime fee, which is why it eventually shows up as a margin problem rather than an acquisition win.

These three numbers, run honestly, will tell you which channels are actually building your firm and which ones are quietly extracting margin you should be keeping.

What this means for your channel mix

Three things, in priority order.

First, renegotiate or wind down the custodian referral channel as soon as you have a credible alternative. It's the highest-cost channel you're running, and almost no RIA has it modeled correctly. You don't need to walk away — but you should know what it's costing you, and you should be building toward a position where you don't depend on it.

Second, build the SEO and content layer now, even if it doesn't produce CAC for 12–18 months. It is the only channel that compounds. Every other channel has roughly stable unit economics across a five-year horizon. SEO, organic content, and LLM-visibility (yes, you should be optimizing for ChatGPT and Perplexity citations now — buyers research there before they ever talk to you) get cheaper per acquisition every quarter, if you run them with real topical authority.

Third, stop running channels you can't measure to the funded-account level. If a channel can't show you CAC-per-funded-account, CAC payback, and CAC-as-percentage-of-LTV, it's a hobby, not a growth channel. Demand the math from your vendors and from your own team.

The compounding channel — and what most RIAs miss about it

The cheapest CAC channel in 2026 isn't a channel. It's an architecture.

A first-party data layer, a closed-loop measurement system, and a content engine that compounds — what we've been calling growth infrastructure — produces CAC numbers that decline quarter over quarter as the system learns. Every other channel has roughly flat unit economics. Infrastructure has improving unit economics. The gap widens over time, and the firms that built it in 2024 and 2025 are now operating with CAC profiles their competitors can't match without rebuilding from scratch.

That doesn't mean you should fire your entire growth team and replace them with a vendor. It means the channel mix question is downstream of an architecture question. If you don't own your data, every channel costs more than it should. If you don't have a closed loop, every campaign starts from zero. Both of those problems are fixable in 2026 in a way they weren't in 2020 — which is why the firms moving now are getting a structural cost advantage, not a tactical one.

CAC is a number. Architecture is the thing that determines what your CAC number can become.

FAQ

What is the average client acquisition cost (CAC) for an RIA in 2026? There isn't a single average that's meaningful. Fully loaded CAC across major channels for RIAs in 2026 typically ranges from $500 to $7,500 per funded client, depending on channel mix, ICP, and operational maturity. The most informative number isn't the average — it's the spread, which signals how well a firm has architected its acquisition system.

Which acquisition channel has the lowest CAC for an RIA? At maturity, SEO and organic content produce the lowest CAC per funded client — typically $300–$1,200 — but require 9–18 months to spool up. True client referrals (existing-client introductions) are also low-cost but volume-constrained. The cheapest channel in the long run is a properly built first-party content and data layer, because its unit economics improve over time.

Why are custodian referral programs considered expensive? Custodian referral programs (Schwab Advisor Network, Fidelity Wealth Advisor Solutions) charge an ongoing percentage of client revenue for the duration of the relationship. On a long client tenure, the implicit cost of acquisition can reach 10–15% of lifetime client revenue, which exceeds nearly every digital channel when measured honestly. Most RIAs don't track this as marketing spend, which is why the channel often appears cheaper than it is.

What CAC math should an RIA principal actually run? Three numbers: CAC-to-funded-account (not cost-per-lead), CAC payback in months (under 18 is healthy), and CAC as a percentage of LTV (1:5 to 1:15 ratio is healthy depending on segment). If a channel can't be measured against all three, it shouldn't be a primary growth channel.

How does AI-powered acquisition compare to traditional channels on CAC? Properly built AI-driven acquisition systems — closed-loop, first-party-data-owned, compliance-embedded — produce CAC numbers that decline quarter over quarter as the system learns. Industry CPL typically runs $190–$300 across paid digital channels. We have an enterprise-grade RIA case running at $70.25 per qualified lead with the architecture in place. The differentiator is the learning loop, not the channel.

Ian J Karnell is the CEO and Co-Founder of VastAdvisor, the AI-native growth infrastructure platform for wealth management. If your firm is rethinking client acquisition economics, request a demo →

Comments